Login or Register for free to create your own customized page of blog posts from your favorite blogs. You can also add blogs by clicking the "Add to MyJacketFlap" links next to the blog name in each post.

Blog Posts by Tag

In the past 7 days

Blog Posts by Date

Click days in this calendar to see posts by day or month

Viewing: Blog Posts Tagged with: European economy, Most Recent at Top [Help]

Results 1 - 6 of 6

How to use this Page

You are viewing the most recent posts tagged with the words: European economy in the JacketFlap blog reader. What is a tag? Think of a tag as a keyword or category label. Tags can both help you find posts on JacketFlap.com as well as provide an easy way for you to "remember" and classify posts for later recall. Try adding a tag yourself by clicking "Add a tag" below a post's header. Scroll down through the list of Recent Posts in the left column and click on a post title that sounds interesting. You can view all posts from a specific blog by clicking the Blog name in the right column, or you can click a 'More Posts from this Blog' link in any individual post.

The 2008 global economic crisis has been the most severe recession since the Great Depression. Notwithstanding its dramatic effects, cross-country analyses on its heterogeneous impacts and its potential causes are still scarce. By analysing the geography of the 2008 crisis, policy-relevant lessons can be learned on how cities and regions react to economic shocks in order to design adequate responses.

Why doesn’t Greece reform? Over the past few years the inability of successive Greek governments to deliver on the demands of international creditors has been a key feature of Greece’s bailout drama. Frustrated observers have pointed to various pathologies of the Greek political system to explain this underperformance.

The limited liability company was one of the most significant inventions of the nineteenth century. The state permitted the incorporation of corporate entities, with many of the legal rights of a person, whilst limiting the liability of their owners for the companies’ debts. Elegantly simple, the limited liability company proved amazingly successful. Unfortunately, the idea was so successful that today the notion has become confused and immensely complex. The entire concept needs reinventing.

Last month, the European Central Bank (ECB) announced its plans to commence a €60 billion (nearly $70 billion) of quantitative easing (QE) through September 2016. In doing so, it is following in the footsteps of American, British, and Japanese central banks all of which have undertaken QE in recent years. Given the ECB’s actions, now is a good time to review quantitative easing. What is it? Why has the ECB decided to adopt this policy now? And what are the likely consequences for Europe and the wider world?

What is quantitative easing (QE)?

Under normal circumstances, central banks undertake monetary policy via open market operations. This typically involves buying (or selling) securities in a short-term money market to lower (or raise) the interest rate prevailing in that market. Central banks are well equipped to do this. They have large inventories of securities that they can easily sell in order withdraw money from the market and push interest rate up. They also have a monopoly on the creation of their particular currency, which they can use to buy securities and push the interest rate down. Open market purchases and sales usually only last for a day or two (through repurchase agreements, or repos), but can be repeated as often as necessary and adjusted in size to achieve the targeted rate.

For an economy that is mired in recession, open market purchases can be a good policy move: buying securities lowers short-term interest rates and increases the money supply. In time, such expansionary monetary policy can also reduce longer-term interest rates, which may stimulate spending on new houses, factories, and equipment, since such investment spending is often made with borrowed money. Expansionary monetary policy will also lead to a decline in the value of the domestic currency on international markets (i.e., depreciation), which will help domestic exports. Too much sustained monetary expansion can lead to inflation, which is one of the main risks of this policy.

In the current economic climate, however, short-term interest rates are already hovering around zero. Although some central banks have flirted with the idea of negative interest rates, there is not much room for conventional expansionary monetary policy to do much good.

Enter quantitative easing. Using quantitative easing, central banks purchase longer-term securities and, unlike open market operations, the purchases are usually permanent instead of for just a few days. This lowers longer-term interest rates. Since individuals and firms that borrow money to invest in homes, factories, and equipment generally do not finance these long-loved assets with overnight borrowing (for mortgages, 15- and 30-year terms are more typical), lowering longer-term interest rates may be a good way to stimulate such long-term investment.

Mario Draghi, President of the ECB, World Economic Forum 2013. CC-BY-SA-2.0 via Wikimedia Commons.

Why now?

The European economy is listless. GDP appears to have grown—just barely—during the year just finished. Although 2014’s performance was an improvement over 2013’s decline in GDP, the EU’s growth forecasts for 2015 and 2016 are far from rosy. The job market is sluggish: EU-wide unemployment was 11.6% in 2014, down slightly from 12.0% in 2013. And a pick-up in inflation, which should accompany growth, was absent in 2014: the authorities have set a 2.0% for inflation; instead prices rose by an anemic 0.4% in 2014. Several countries have made progress toward much-needed structural reform; however, it is not clear that such reforms alone will get the European economy out of the doldrums anytime soon.

Other dangers facing the European economy also argue in favor of quantitative easing. To the east, tensions with Russia could flare at any time. The terrorist attacks in France have given a boost to right-wing parties throughout Europe, another threat to stability. And the election victory of the anti-austerity Syriza party in Greece, suggests that relations between Greece and the EU are about to get rockier.

What are the consequences?

Quantitative easing will strengthen Europe’s wobbly recovery. The announcement quickly lifted European stock markets—the Euro Stoxx 50-share index rose 1.6% on the news. Lower longer-term interest rates should encourage more borrowing and investment spending. And QE will lead to a continued depreciation in the value of the euro, already at a decade-low against the US dollar, which will make European exports more competitive in world markets. The results will not be so pleasant for American exports, since the euro’s depreciation will cut into recent American export growth, which has benefitted from three rounds of American QE, the last of which ended a few months ago.

Quantitative easing will not sit well with all Euro-zone countries. Germany, which is economically far more robust than its European partners, is not a fan of QE. Memories of a destructive hyperinflation in the 1920s still linger in the national consciousness, lead Germans to be far more skeptical of a potentially inflationary policy that they see as bailing out their more profligate neighbors at their expense.

Finally, the European Central Bank has not said exactly which bonds it will buy. When the US Federal Reserve undertook QE, it had a wide variety of Treasury securities to purchase. Given the high credit-worthiness of the US government and the fact that the market for US Treasury securities is the most liquid market in the world, it was not difficult to find suitable securities to purchase. Will the ECB buy the debt of the fiscally weak euro-zone nations and put their balance sheet at risk? Or will it restrict its purchases to only the most credit worthy countries and risk the ire of the citizens from less well-heeled nations?

Despite these legitimate concerns, Europe’s weak economic performance requires bold action. Quantitative easing is an important step in the right direction.

Featured image credit: Growing Euros, by Images_of_money. CC-BY-2.0 via Flickr.

Bliss was it in that dawn to be alive

But to be young was very heaven!

– William Wordsworth on the French Revolution

I was not that young when New Europe’s transition began in 1989, but I was there: in Poland at the start of the 1990s and in Russia during its 1998 crisis and after, in both cases as the resident economist for the World Bank. This year is the 25th anniversary of New Europe’s transition and the sixth year of Old Europe’s growth-cum-sovereign debt crisis. Old Europe can learn from New Europe: first, about getting government debt dynamics under control if you want growth. Second, about implementing the policy trio of hard budgets, competition and competitive real exchange rates to keep debt dynamics under control and get growth. The contrasting experiences of Poland and Russia underline these lessons (Andrei Shleifer’s take on the transition lessons can be found here).

Poland started with a big bang in 1990, but ran into political roadblocks on the privatization of large state enterprises. It achieved single-digit inflation only in 1998. Between 1995 and 1998, Russia did the opposite. By early 1998, privatization was done and single-digit inflation achieved. But while Poland started growing in 1992 and has one of the most enviable growth records in Europe, Russia suffered a huge crisis in August 1998 after which it was forced to adopt the same policy agenda as Poland.

The first difference is that Poland quickly established fiscal discipline and capitalized on the debt reduction it received from the Paris and London Clubs to get government debt dynamics under control. Russia lost control over its government debt dynamics even as the central bank obsessively squeezed inflation out.

The second difference is that Poland instantly hardened budgets by slashing subsidies to state-owned enterprises (SOEs) and subsequently restricting bank lending to loss-making SOEs. It summarily increased competition by liberalizing imports, but was careful to avoid a large real appreciation by devaluing the zloty 17 months after the big bang, and then moving to a flexible exchange rate. The first two elements of this micropolicy trio, hard budgets and competition, forced SOEs to raise efficiency even before privatization. The third, competitive real exchange rates, gave them breathing space. Indeed, SOEs were in the forefront of the economic recovery which began in late 1992, ensuring that debt dynamics would remain sustainable. This does not mean privatization was irrelevant: SOE managers were anticipating it and expecting to benefit from it; but the immediate spur was definitely the micropolicy trio.

In contrast, Russia’s privatized manufacturing companies were coddled by budgetary subsidies and large subsidies implicit in the noncash settlements for taxes and energy payments that sprouted as real interest rates rose to astronomical levels. Persistent fiscal deficits and low credibility pushed nominal interest rates sky high even as the exchange rate was fixed in 1995 to bring inflation down. The resulting soft budgets, high real interest rates and real appreciation made asset stripping easier than restructuring enterprises, killing growth. Tax shortfalls became endemic, forcing increasingly expensive borrowing that placed government debt on an explosive trajectory and made the August 1998 devaluation, default and debt restructuring inevitable. But this shut the country out of the capital markets, at last hardening budgets. The real exchange rate depreciated massively, leading to a 5% rebound in real GDP in 1999 (against initial expectations of a huge contraction) as moribund firms became competitive and domestic demand switched from imports to domestic products. This policy mix was maintained after oil prices recovered in 2000, ensuring sustainable debt dynamics.

Old Europe, especially the periphery, can learn a lot from the above. Take Italy. By 2013, its real exchange rate had appreciated over 3% relative to 2007, while real GDP had contracted over 8%. The government’s debt-to-GDP ratio increased by 30 percentage points (and is projected to climb to 135% by the end of this year), while youth unemployment went from 20% to 40% over the same period! Italy has no control over the nominal exchange rate and lowering indebtedness through fiscal austerity will worsen already weak growth prospects. Indeed, Italy has slipped back into recession in spite of interest rates at multi-century lows and forbearance on fiscal austerity.

The counter argument is that indebtedness and competitiveness don’t look that bad for the Eurozone as a whole. However, this argument is vacuous without debt mutualisation, a fiscal union and a banking union with a common fiscal backstop, the latter to prevent individual sovereigns, such as Ireland and Spain, from having to shoulder the costs of fixing their troubled banks; the recent costly bailout of Banco Espirito Santo by Portugal is a timely reminder. Besides, Germany has to be willing to cross-subsidize the periphery. Even then, this would only be a start. As a recent IMF report warns, the Eurozone is at risk of stagnation from insufficient demand (linked to excessive debt), a weak and fragmented banking system and stalled structural reform required for increasing competition and raising productivity. Debtor countries are hamstrung by insufficient relative price adjustment (read “insufficient real depreciation”).

The corrective agenda for the Eurozone has much in common with the “debt restructuring-cum-micro policy trio” agenda emerging from the Polish and Russian transition experience. The question is whether the Eurozone can have meaningful growth prospects based on banking and structural reform without an upfront debt restructuring. The answer from New Europe’s experience is “No.” Debt restructuring will result in a temporary loss of confidence and possibly even a recession; but it will also lead to a large real depreciation and harden budgets, spurring governments to complete structural reform, thereby laying the foundation for a brighter future. The key is not the debt restructuring, but whether government behaviour changes credibly for the better following it. As the IMF report observes, progress “may be prone to reform fatigue” with the rally in financial markets. In other words, the all-time lows in interest rates set in train by ECB President Draghi’s July 2012 pledge to do whatever it takes to save the euro is fuelling procrastination even as indebtedness grows and growth prospects dim. Rising US interest rates as the recovery there takes hold and the growing geopolitical risk over Ukraine, which will hurt the Eurozone more than the US, only worsen the picture. The Eurozone has a stark choice: take the pain now or live with a stagnant future, meaning its youth have fewer jobs today and more debt to pay off tomorrow.

Because Europe accounts for nearly a quarter of the world’s economic output, this question is important not only to Europeans, but to Africans, Asians, Americans (both North and South), and Australians as well. Those who forecast that the United States’s relatively anemic five-year-old recovery is poised to become stronger almost always include the caveat “unless, of course, Europe implodes.”

So, can we stop worrying about Europe?

Recent signs have been encouraging.

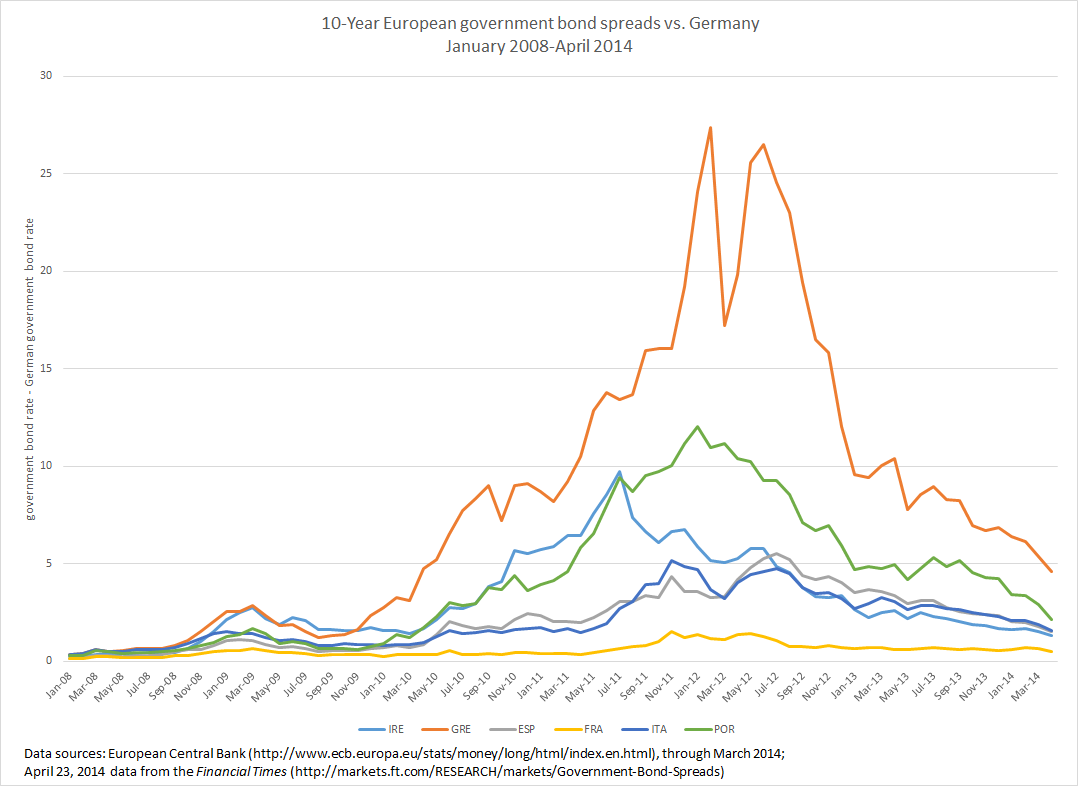

Consider the following graph, which shows the spread between the yields on the 10-year bonds of several European countries and those of the German government. Because the German government’s finances are relatively healthy—and Germany is thus viewed as being quite likely to pay back what it owes—it is able to borrow money more cheaply than most of its neighbors. For 10 years loans, the German government pays interest of about 1.5%, which is among the lowest rates in Europe.

Before the European sovereign debt crisis erupted 2009, spreads were not especially wide. In 2008, the Greek government paid between 0.25-0.75% more to borrow money for 10 years than the German government. When the sorry state of the Greek government’s finances became public, however, the spread between Greek and German yields soared to more than 20% and the European Union (EU) and the International Monetary Fund (IMF) were called in to bail out the Greek government. Ireland, Portugal, and Spain also received rescue packages (as did Cyprus), while Italy appeared to be headed down the same road. Note the wide spreads between these governments’ borrowing costs and those of the fiscally virtuous Germans.

During the last year or so, Greek, Irish, Portuguese, and Spanish spreads have shrunk considerably — not to their pre-crisis levels, but far below their sky-high levels of 2010-2012 — suggesting that doubts about the sustainability of European governments’ debts is receding. The decline in spreads is due in part to the austerity measures adopted as a condition of the EU/IMF bailouts, which have improved the budget outlook among the fiscally weaker countries. German Chancellor Angela Merkel’s April visit to Greece was widely seen as an effort to show support for fiscal austerity and economic restructuring adopted by the Greek Prime Minister Antonis Samaras.

Angela Merkel – Αντώνης Σαμαράς, 2012. Photo by Αντώνης Σαμαράς Πρωθυπουργός της Ελλάδας. CC BY-SA 2.0 via Wikimedia Commons.

In other positive news, Markit’s European purchasing manager’s composite index for March (released on 23 April 2014), which is considered a proxy for economic output, rose to a nearly three-year high. The index shows a continuous expansion of business activity since last July and forecasts that a backlog of work will lead to further growth in May.

Despite these positive signs, Europe is not out of the woods.

Unemployment remains stubbornly high, due, in part, to austerity: over 25% in Greece and Spain; over 15% in Portugal and Cyprus; and over 10% in France, Ireland, Italy, and a number of other countries.

Although prices are rising slightly in the European Union on average, Greece, Spain, Portugal and a few other European countries are experiencing deflation. Moreover, overall inflation in the EU is below that in the United States, leading the euro to appreciate by between 2-3% against the dollar since the beginning of 2014 and putting a crimp in European exports. Further, Europe’s flirtation with deflation increases the real burden on debtors. During inflationary times, debtors are able to repay their debts in money that is losing its value; deflation forces debtors to repay in money that is gaining in value.

The European economy is improving. But several indicators show that plenty can still go wrong. So let’s not stop worrying yet.

Subscribe to the OUPblog via email or RSS.

Subscribe to only business and economics articles on the OUPblog via email or RSS.

Image credit: Graph courtesy of Richard Grossman. Used with permission.