JacketFlap connects you to the work of more than 200,000 authors, illustrators, publishers and other creators of books for Children and Young Adults. The site is updated daily with information about every book, author, illustrator, and publisher in the children's / young adult book industry. Members include published authors and illustrators, librarians, agents, editors, publicists, booksellers, publishers and fans. Join now (it's free).

Sort Blog Posts

Sort Posts by:

Suggest a Blog

Enter a Blog's Feed URL below and click Submit:

Most Commented Posts

In the past 7 days

Recent Posts

(tagged with 'Economic Policy with Richard S. Grossman')

Login or Register for free to create your own customized page of blog posts from your favorite blogs. You can also add blogs by clicking the "Add to MyJacketFlap" links next to the blog name in each post.

Blog Posts by Tag

In the past 7 days

Blog Posts by Date

Click days in this calendar to see posts by day or month

Viewing: Blog Posts Tagged with: Economic Policy with Richard S. Grossman, Most Recent at Top [Help]

Results 1 - 22 of 22

How to use this Page

You are viewing the most recent posts tagged with the words: Economic Policy with Richard S. Grossman in the JacketFlap blog reader. What is a tag? Think of a tag as a keyword or category label. Tags can both help you find posts on JacketFlap.com as well as provide an easy way for you to "remember" and classify posts for later recall. Try adding a tag yourself by clicking "Add a tag" below a post's header. Scroll down through the list of Recent Posts in the left column and click on a post title that sounds interesting. You can view all posts from a specific blog by clicking the Blog name in the right column, or you can click a 'More Posts from this Blog' link in any individual post.

A few weeks ago, I received an e-mail inviting me to sign a statement drafted by a group calling itself “Economists Concerned by Hillary Clinton’s Economic Agenda.” The statement, a vaguely worded five paragraph denunciation of Democratic policies (and proposed policies) is unremarkable — as are the authors, a collection of reliably conservative policy makers and commentators whose support for Donald Trump appear with some regularity in the media.

Inspired by the 11 Tony awards won by the smash Broadway hit Hamilton, last month I wrote about Alexander Hamilton as the father of the US national debt and discussed the huge benefit the United States derives from having paid its debts promptly for more than two hundred years. Despite that post, no complementary tickets to Hamilton have arrived in my mailbox. And so this month, I will discuss Hamilton’s role as the founding father of American central banking.

have not yet seen Lin-Manuel Miranda’s hit Broadway show Hamilton. I feel badly about this for three reasons. First, Miranda is a 2002 Wesleyan graduate, a loyal and generous alumnus who gave a great commencement speech in 2015 and remains solidly committed to the university. Second, the music and lyrics are, quite simply, amazing. Third, as an economic historian, it is heartening to see one of America’s economic heroes make it to Broadway.

have not yet seen Lin-Manuel Miranda’s hit Broadway show Hamilton. I feel badly about this for three reasons. First, Miranda is a 2002 Wesleyan graduate, a loyal and generous alumnus who gave a great commencement speech in 2015 and remains solidly committed to the university. Second, the music and lyrics are, quite simply, amazing. Third, as an economic historian, it is heartening to see one of America’s economic heroes make it to Broadway.

In the 1983 movie The Right Stuff, during a test of wills between the Mercury Seven astronauts and the German scientists who designed the spacecraft, the actor playing astronaut Gordon Cooper asks: “Do you boys know what makes this bird fly?” Before the hapless engineer can reply with a long-winded scientific explanation, Cooper answers: “Funding!” If an economist were asked, “Do you know what makes this economy fly?” the answer, in one word, would be “trust.”

The Chinese New Year begins on 8 February, ushering out the year of the sheep (or goat, or ram) and bringing in the year of the monkey. People in China will enjoy a week-long vacation and will celebrate with dragon dances and fireworks. Given the financial fireworks emanating from China, this is a good time to briefly review some of the major economic news coming out of the Middle Kingdom.

Economists are better at history than forecasting. This explains why financial journalists sound remarkably intelligent explaining yesterday’s stock market activity and, well, less so when predicting tomorrow’s market movements. And why I concentrate on economic and financial history. Since 2015 is now in the history books, this is a good time to summarize a few main economic trends of the preceding year.

Seven years ago this month the federal funds rate—a key short-term interest rate set by the Federal Reserve—was lowered below 0.25%. It has remained there ever since.Lowering the fed funds rate to rock-bottom levels did not come as a surprise. The sub-prime mortgage crisis led to a severe economic contraction, the Great Recession, and Federal Reserve policy makers used low interest rates—among other tools—in an effort to revive the economy.

With elections just about a year away, Americans can expect to hear a lot about regulation during the next twelve months—most of it from Republicans and most of it scathing. Republican frontrunner Donald Trump typifies the GOP’s attitude toward regulation.

t the conclusion of the mid-September meeting of the Federal Open Market Committee (FOMC), the Federal Reserve announced its decision to leave its target interest rate unchanged through the end of this month. Although some pundits had predicted that the Fed might use the occasion of August’s decline in the unemployment rate (to 5.1 percent from 5.3 percent in July), to begin its long-awaited monetary policy tightening, those forecasts left out one crucial fact.

The next time you are slipping the valet a couple of folded dollar bills, take a good look at those George Washingtons. You might never see them again. Every few years, there is a renewed push for the United States to replace the dollar bill with its shiny cousin, the one dollar coin.

One of the most striking structural weaknesses uncovered by the euro crisis is the lack of consistent banking regulation and supervision in Europe. Although the European Banking Authority has existed since 2011, its influence is often trumped by national authorities. And many national governments within the European Union do not seem anxious to submit their financial institutions to European-wide regulation and supervision.

The industrialized world is currently moving through a period of ultra-low interest rates. The main benchmark interest rates of central banks in the United States, the United Kingdom, Japan, and the euro-zone are all 0.50% or less. The US rate has been near zero since December 2008; the Japanese rate has been at or below 0.50% since 1995. Then there are the central banks that have gone negative: the benchmark rates in Denmark, Sweden, and Switzerland are all below zero. Other short-term interest rates are similarly at rock-bottom levels, or below.

Last month, the European Central Bank (ECB) announced its plans to commence a €60 billion (nearly $70 billion) of quantitative easing (QE) through September 2016. In doing so, it is following in the footsteps of American, British, and Japanese central banks all of which have undertaken QE in recent years. Given the ECB’s actions, now is a good time to review quantitative easing. What is it? Why has the ECB decided to adopt this policy now? And what are the likely consequences for Europe and the wider world?

What is quantitative easing (QE)?

Under normal circumstances, central banks undertake monetary policy via open market operations. This typically involves buying (or selling) securities in a short-term money market to lower (or raise) the interest rate prevailing in that market. Central banks are well equipped to do this. They have large inventories of securities that they can easily sell in order withdraw money from the market and push interest rate up. They also have a monopoly on the creation of their particular currency, which they can use to buy securities and push the interest rate down. Open market purchases and sales usually only last for a day or two (through repurchase agreements, or repos), but can be repeated as often as necessary and adjusted in size to achieve the targeted rate.

For an economy that is mired in recession, open market purchases can be a good policy move: buying securities lowers short-term interest rates and increases the money supply. In time, such expansionary monetary policy can also reduce longer-term interest rates, which may stimulate spending on new houses, factories, and equipment, since such investment spending is often made with borrowed money. Expansionary monetary policy will also lead to a decline in the value of the domestic currency on international markets (i.e., depreciation), which will help domestic exports. Too much sustained monetary expansion can lead to inflation, which is one of the main risks of this policy.

In the current economic climate, however, short-term interest rates are already hovering around zero. Although some central banks have flirted with the idea of negative interest rates, there is not much room for conventional expansionary monetary policy to do much good.

Enter quantitative easing. Using quantitative easing, central banks purchase longer-term securities and, unlike open market operations, the purchases are usually permanent instead of for just a few days. This lowers longer-term interest rates. Since individuals and firms that borrow money to invest in homes, factories, and equipment generally do not finance these long-loved assets with overnight borrowing (for mortgages, 15- and 30-year terms are more typical), lowering longer-term interest rates may be a good way to stimulate such long-term investment.

Mario Draghi, President of the ECB, World Economic Forum 2013. CC-BY-SA-2.0 via Wikimedia Commons.

Why now?

The European economy is listless. GDP appears to have grown—just barely—during the year just finished. Although 2014’s performance was an improvement over 2013’s decline in GDP, the EU’s growth forecasts for 2015 and 2016 are far from rosy. The job market is sluggish: EU-wide unemployment was 11.6% in 2014, down slightly from 12.0% in 2013. And a pick-up in inflation, which should accompany growth, was absent in 2014: the authorities have set a 2.0% for inflation; instead prices rose by an anemic 0.4% in 2014. Several countries have made progress toward much-needed structural reform; however, it is not clear that such reforms alone will get the European economy out of the doldrums anytime soon.

Other dangers facing the European economy also argue in favor of quantitative easing. To the east, tensions with Russia could flare at any time. The terrorist attacks in France have given a boost to right-wing parties throughout Europe, another threat to stability. And the election victory of the anti-austerity Syriza party in Greece, suggests that relations between Greece and the EU are about to get rockier.

What are the consequences?

Quantitative easing will strengthen Europe’s wobbly recovery. The announcement quickly lifted European stock markets—the Euro Stoxx 50-share index rose 1.6% on the news. Lower longer-term interest rates should encourage more borrowing and investment spending. And QE will lead to a continued depreciation in the value of the euro, already at a decade-low against the US dollar, which will make European exports more competitive in world markets. The results will not be so pleasant for American exports, since the euro’s depreciation will cut into recent American export growth, which has benefitted from three rounds of American QE, the last of which ended a few months ago.

Quantitative easing will not sit well with all Euro-zone countries. Germany, which is economically far more robust than its European partners, is not a fan of QE. Memories of a destructive hyperinflation in the 1920s still linger in the national consciousness, lead Germans to be far more skeptical of a potentially inflationary policy that they see as bailing out their more profligate neighbors at their expense.

Finally, the European Central Bank has not said exactly which bonds it will buy. When the US Federal Reserve undertook QE, it had a wide variety of Treasury securities to purchase. Given the high credit-worthiness of the US government and the fact that the market for US Treasury securities is the most liquid market in the world, it was not difficult to find suitable securities to purchase. Will the ECB buy the debt of the fiscally weak euro-zone nations and put their balance sheet at risk? Or will it restrict its purchases to only the most credit worthy countries and risk the ire of the citizens from less well-heeled nations?

Despite these legitimate concerns, Europe’s weak economic performance requires bold action. Quantitative easing is an important step in the right direction.

Featured image credit: Growing Euros, by Images_of_money. CC-BY-2.0 via Flickr.

Burdensome, costly, and—let’s face it—just plain stupid government regulation is all around us. And even well-meaning, reasonably well-designed regulations can impose costs all out of proportion with their benefits.

Consider the Family Educational Rights and Privacy Act (FERPA) (20 U.S.C. § 1232g; 34 CFR Part 99), a Federal law that has the admirable goal of protecting the privacy of student education records. My colleagues and I were recently informed by university officials that we may no longer leave corrected student assignments in a public place for them to pick up, because such materials are part of a student’s confidential record.

This would be a sensible rule if it applied only to exams, term papers, or other major assignments. However, the rule also applies to homework assignments which account for a trivial portion of a student’s actual course grade and are mostly just checked for completion. We will most likely devise a time-consuming work-around: generating random code numbers for each student and using those code numbers in place of names on all of their assignments. The alternative would be to return each problem set individually which, in a class of 100 students, would take too much time away from teaching and learning.

Making fun of these regulations, the politicians who make them, and the regulators and lawyers who make sure that they are adhered to is good sport—and the only compensation we get for putting up with them. Our distain for bad regulations, however, should not get in the way of recognizing that there are also good regulations.

Dodd-Frank was passed in the aftermath of the US subprime crisis. The text of the law is 848 pages long and contains a large number of provisions—some good, some bad, and some that have not yet been implemented. Section 716 of the law regulates “swaps,” one of the risker types of derivative securities which played an important role in the subprime meltdown. Known as the “Swap Push-out Rule,” section 716 prohibited institutions that dealt in these securities from receiving “federal assistance,” including advances from the Federal Reserve or FDIC insurance or guarantees.

In other words, if your institution got into trouble by dealing in these very risky securities, the feds would not bail you out with taxpayer money. Further, you could not pay for these securities by using money that you held—at very low cost–by taking federally insured deposits. Under section 716, banks had to “push out” these derivative out to affiliated—but uninsured—firms.

There has been a fair bit of fallout since the rule was revised. It has been alleged that the wording—originally contained in legislation passed by the House (but defeated in the Senate) last year—was written by bank lobbyists, in particular those on Citigroup’s payroll. Few lawmakers have been standing up to take credit for the latest attempt to revise section 716, although former Fed chair Ben Bernanke is on record as having supported some alteration to the regulation. Opponents of the revision come from the right and left, and include Senators Elizabeth Warren (D-MA), David Vitter (R-LA), and Sherrod Brown (D-OH). The White House opposed the measure, as did the Vice Chair of the Federal Deposit Corporation, former Federal Reserve Bank of Kansas City President Thomas Hoenig.

The amendment of section 716 is bad news for America’s future financial stability and the American taxpayer. Banks will now be able to use low-cost federally insured deposits to engage in risky swap transactions. And, when these transactions land them in trouble, they will be able to turn to the federal government to bail them out.

The problems generated by the revision of section 716 of Dodd-Frank can be reversed. All that is needed is for the authorities to force institutions that deal in these swap transactions to back them with enough capital to ensure that bank shareholders–and not taxpayers—will pay the price if the transactions sour. Given Congress’s willingness to throw section 716 overboard, such a reform is extremely unlikely.

For those addicted to politics, newspapers and magazines have long provided abundant, sometimes even insightful coverage. During the last hundred years, print outlets have been supplemented by radio, then television, then 24/7 cable TV news. And with the growth of the internet, consumers of political news now have access to more analysis than ever.

One analytical tool that the politics-following public will not have access to this year is Intrade, an on-line political prediction market. Political prediction markets work very much like financial markets. Investors “buy” a futures contract on a particular candidate; if that candidate wins, the contract pays a set amount (typically $1); if the candidate loses, the contract becomes worthless. The price of candidates’ contracts vary between zero and $1, rising and falling with their political fortunes—and their probability of winning. You can see a graph of Obama and Romney contracts in the months preceding the 2012 election here.

Organized political betting markets have existed in the United States since the early days of the Republic. According to a 2003 paper by Rhode and Strumpf, during the late 19th and early 20th centuries wagering on political outcomes was common and market prices of contracts were often published in newspapers along with those of more conventional financial investments. Rhode and Strumpf note that at the Curb Exchange in New York, the total sum placed on political contracts sometimes exceeded trading in stocks and bonds.

Political betting markets became less popular around 1940. Betting on election outcomes no doubt continued to take place, but it was a much less high-profile affair.

Modern political prediction markets emerged with the establishment in 1988 of the Iowa Electronic Markets (IEM), a not-for-profit small-scale exchange run by the College of Business at the University of Iowa. The IEM was created as a teaching and research tool to both better understand how markets interpret real-world events and to study individual trading behavior in a laboratory setting. The IEM usually offers only a few contracts at any one time and investors are allowed to invest a relatively small amount of money. As of mid-October, the Iowa markets—like the polls more generally—were predicting that the Republicans will gain seats in the House and gain control of the Senate.

Wooden Ballot Box, by the Smithsonian Institution. Public domain via Wikimedia Commons.

An important feature of political prediction markets—like financial markets—is that they are efficient at processing information: the prices generated in those markets are a distillation of the collective wisdom of market participants. A desire to harness the market’s ability to process information led to an abortive attempt by the Defense Advanced Research Projects Agency in 2003 to create the Policy Analysis Market, which would allow individuals to bet on the likelihood of political and military events—including assassinations and terrorist attacks–taking place in the Middle East. The idea was that by processing information from a variety disparate sources, monitoring the prices of various contracts would help the defense establishment identify hot-spots before they became hot. The project was hastily cancelled after Congress and the public expressed outrage that the government was planning to provide the means (and motive) to speculate on—and possibly profit from–terrorism.

Another, longer-lived—and for a time, quite popular–prediction market was Intrade.com. This Dublin-based company was established in 1999. At first, it specialized in sports betting, but soon expanded to include an extensive menu of political markets. During recent elections, Intrade operated prediction markets on the presidential election outcome at the national level, the contest for each state’s electoral votes, individual Senate races, as well as a number of other political races in the US and overseas. Thus, Intrade offered a far variety of betting options than the IEM.

Intrade was forced to close last year when the US Commodities Futures Trading Commission (CFTC) filed suit against it for illegally allowing Americans to trade options (by contract, the IEM secured written opinions in 1992 and 1993 from the CFTC that it would not take action against IEM, because of that market’s non-profit, educational nature). The CFTS’s threat to Intrade’s largest customer base very quickly led to a dramatic drop-off in visitors to the site, which subsequently closed. Alternative off-shore betting markets have entered the political markets (e.g., Betfair), but their offerings pale by comparison with those formerly offered by Intrade and are probably too small at present to spur the CFTC to action.

I regret the loss of Intrade, but not because I used their services—I didn’t. Given the federal government’s generally hostile view toward internet gambling, I felt it was prudent to abstain. Plus, having placed a two-pound wager on a Parliamentary election with a bookmaker when I lived in England many years ago convinced me that an inclination to bet with the heart, rather than the head, makes for an unsuccessful gambler.

No, I miss Intrade because it provided a nice summary of many different political campaigns. Sure, there are plenty of on-line tools today that provide a wide array of expert opinion and sophisticated polling data. Still, as an economist, I enjoyed the application of the mechanisms usually associated with financial markets to politics and observing how political news generated fluctuations in those markets. No other single source today does that for as many political races as Intrade did.

Feature image credit: Stock market board, by Katrina.Tuiliao. CC-BY-2.0 via Wikimedia Commons.

On September 18, Scots will go to the polls to vote on the question “Should Scotland be an independent country?” A “yes” vote would end the political union between England and Scotland that was enacted in 1707.

The main economic reasons for independence, according to the “Yes Scotland” campaign, is that an independent Scotland would have more affordable daycare, free university tuition, more generous retirement and health benefits, less burdensome regulation, and a more sensible tax system.

As a citizen of a former British colony, it is tempting to compare the situation in Scotland with those of British colonies and protectorates that gained their independence, such as the United States, India/Pakistan, and a variety of smaller countries in Africa, Asia, and the Americas, although such a comparison is unwarranted.

Historically, independence movements have been motivated by absence of representation in the institutions of government, discrimination against the local population, and economic grievances. These arguments do not hold in the Scottish case.

Scotland is an integral part of the United Kingdom. It is represented in the British Parliament in Westminster, where it holds 9% of the seats—fair representation, considering that Scotland’s population is a bit less than 8.5% of total UK population.

Scotland does have a considerable measure of self-government. A Scottish Parliament, created in 1998, has authority over issues such as health, education, justice, rural affairs, housing and the environment, and some limited authority over tax rates. Foreign and defense policy remain within the purview of the British government.

Scots do not seem to have been systematically discriminated against. At least eight prime ministers since 1900, including recent ex-PMs Tony Blair and Gordon Brown, were either born in Scotland or had significant Scottish connections.

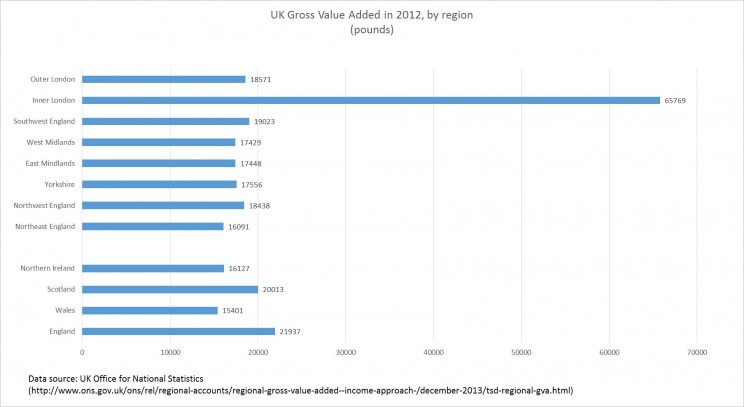

Scotland is about as prosperous as the rest of the UK, with output per capita greater than those of Wales, Northern Ireland, and England outside of London (see figure).

Because the referendum asks only whether Scotland should become independent and contains no further details on how the break-up with the UK would be managed, it is important to consider some key economic issues that will need to be tackled should Scotland declare its independence.

Graph showing UK Gross Value, created by Richard S. Grossman with data from the UK Office of National Statistics.

Since Scotland already has a parliament that makes many spending and taxing decisions, we know something about Scottish fiscal policy. According to the World Bank figures, excluding oil (a resource that is expected to decline in importance in coming decades), Scotland’s budget deficit as a share of gross domestic product already exceeds those of fiscally troubled neighbors Greece, Spain, Ireland, Portugal, and Italy. Given the “Yes” campaign’s promise to make Scotland’s welfare system even more generous, the fiscal sustainability of an independent Scotland’s is unclear.

As in any divorce, the parties would need to divide their assets and liabilities.

The largest component of UK liabilities are represented by the British national debt, recently calculated at around £1.4 trillion ($2.4 trillion), or about 90 percent of UK GDP. What share of this would an independent Scotland “acquire” in the break-up?

Assets would also have to be divided. One of the greatest assets—North Sea oil—may be more straightforward to divide given that the legislation establishing the Scottish Parliament also established a maritime boundary between England and Scotland, although this may be subject to negotiation. But what about infrastructure in England funded by Scottish taxes and Scottish infrastructure paid for with English taxes?

An even more contentious item is the currency that would be used by an independent Scotland. The pro-independence camp insists that an independent Scotland would remain in a monetary union with the rest of the UK and continue to use the British pound. And, in fact, there is no reason why an independent Scotland could not declare the UK pound legal tender. Or the euro. Or the US dollar, for that matter.

The problem is that the “owner” of the pound, the Bank of England, would be under no obligation to undertake monetary policy actions to benefit Scotland. If a sluggish Scottish economy is in need of loose monetary policy while the rest of the UK is more concerned about inflation, the Bank of England would no doubt carry out policy aimed at the best interests of the UK—not Scotland.

If a Scottish financial institution was on the point of failure, would the Bank of England feel duty-bound to lend pounds? As lender of last resort in England, the Bank has an obligation to supervise—and assist, via the extension of credit—troubled English financial institutions. It seems unlikely that an independent Scotland would allow its financial institutions to be supervised and regulated by a foreign power—nor would that power be morally or legally required to extend the UK financial safety net to Scotland.

At the time of this writing (the second half of August), the smart money (and they do bet on these things in Britain) is on Scotland saying no to independence, although poll results released on August 18 found a surge in pro-independence sentiment. Whatever the polls indicate, no one is taking any chances. Several Scottish-based financial companies are establishing themselves as corporations in England so that, in the case of independence they will not be at a foreigner’s disadvantage vis-à-vis their English clients. Given the economic uncertainty generated by the vote, the sooner September 18 comes, the better for both Scotland and the UK.

Headline image credit: Scottish Parliament building, by Jamieli. Public domain via Wikimedia Commons.

As an early-stage graduate student in the 1980s, I took a summer off from academia to work at an investment bank. One of my most eye-opening experiences was discovering just how much effort Wall Street devoted to “Fed watching”, that is, trying to figure out the Federal Reserve’s monetary policy plans.

If you spend any time following the financial news today, you will not find that surprising. Economic growth, inflation, stock market returns, and exchange rates, among many other things, depend crucially on the course of monetary policy. Consequently, speculation about monetary policy frequently dominates the financial headlines.

Back in the 1980s, the life of a Fed watcher was more challenging: not only were the Fed’s future actions unknown, its current actions were also something of a mystery.

You read that right. Thirty years ago, not only did the Fed not tell you where monetary policy was going but, aside from vague statements, it did not say much about where it was either.

Given that many of the world’s central banks were established as private, profit-making institutions with little public responsibility, and even less public accountability, it is unremarkable that central bankers became accustomed to conducting their business behind closed doors. Montagu Norman, the governor of the Bank of England between 1920 and 1944 was famous for the measures he would take to avoid of the press. He adopted cloak and dagger methods, going so far as to travel under an assumed name, to avoid drawing unwanted attention to himself.

The Federal Reserve may well have learned a thing or two from Norman during its early years. The Fed’s monetary policymaking body, the Federal Open Market Committee (FOMC), was created under the Banking Act of 1935. For the first three decades of its existence, it published brief summaries of its policy actions only in the Fed’s annual report. Thus, policy decisions might not become public for as long as a year after they were made.

Limited movements toward greater transparency began in the 1960s. By the mid-1960s, policy actions were published 90 days after the meetings in which they were taken; by the mid-1970s, the lag was reduced to approximately 45 days.

Since the mid-1990s, the increase in transparency at the Fed has accelerated. The lag time for the release of policy actions has been reduced to about three weeks. In addition, minutes of the discussions leading to policy actions are also released, giving Fed watchers additional insight into the reasoning behind the policy.

More recently, FOMC publicly announces its target for the Federal Funds rate, a key monetary policy tool, and explains its reasoning for the particular policy course chosen. Since 2007, the FOMC minutes include the numerical forecasts generated by the Federal Reserve’s staff economists. And, in a move that no doubt would have appalled Montagu Norman, since 2011 the Federal Reserve chair has held regular press conferences to explain its most recent policy actions.

The Fed is not alone in its move to become more transparent. The European Central Bank, in particular, has made transparency a stated goal of its monetary policy operations. The Bank of Japan and Bank of England have made similar noises, although exactly how far individual central banks can, or should, go in the direction of transparency is still very much debated.

Despite disagreements over how much transparency is desirable, it is clear that the steps taken by the Fed have been positive ones. Rather than making the public and financial professionals waste time trying to figure out what the central bank plans to do—which, back in the 1980s took a lot of time and effort and often led to incorrect guesses—the Fed just tells us. This make monetary policy more certain and, therefore, more effective.

Greater transparency also reduces uncertainty and the risk of violent market fluctuations based on incorrect expectations of what the Fed will do. Transparency makes Fed policy more credible and, at the same time, pressures the Fed to adhere to its stated policy. And when circumstances force the Fed to deviate from the stated policy or undertake extraordinary measures, as it has done in the wake of the financial crisis, it allows it to do so with a minimum of disruption to financial markets.

Montagu Norman is no doubt spinning in his grave. But increased transparency has made us all better off.

Subscribe to the OUPblog via email or RSS.

Subscribe to only business and economics articles on the OUPblog via email or RSS.

Image credits: (1) Federal Reserve, Washington, by Rdsmith4. CC-BY-SA-2.5 via Wikimedia Commons. (2) European Central Bank, by Eric Chan. CC-BY-2.0 via Wikimedia Commons.

What do the Irish famine and the euro crisis have in common?

The famine, which afflicted Ireland during 1845-1852, was a humanitarian tragedy of massive proportions. It left roughly one million people—or about 12 percent of Ireland’s population—dead and led an even larger number to emigrate.

The euro crisis, which erupted during the autumn of 2009, has resulted in a virtual standstill in economic growth throughout the Eurozone in the years since then. The crisis has resulted in widespread discontent in countries undergoing severe austerity and in those where taxpayers feel burdened by the fiscal irresponsibility of their Eurozone partners.

Despite these widely differing circumstances, these crises have an important element in common: both were caused by economic policies that were motivated by ideology rather than cold hard economic analysis.

The Irish famine came about when the infestation of a fungus, Phythophthora infestans, led to the decimation of the potato crop. Because the Irish relied so heavily on potatoes for food, this had a devastating effect on the population.

At the time of the famine, Ireland was part of the United Kingdom. Britain’s Conservative government of the time, led by Prime Minister Sir Robert Peel, swiftly undertook several measures aimed at alleviating the crisis, including arranging a large shipment of grain from the United States in order to offer temporary relief to those starving in Ireland.

More importantly, Peel engineered a repeal of the Corn Laws, a set of tariffs that kept grain prices high. Because the Corn Laws benefitted Britain’s landed aristocracy—an important constituency of the Conservative Party, Peel soon lost his job and was replaced as prime minister by the Liberal Party’s Lord John Russell.

Russell and his Liberal Party colleagues were committed to an ideology that opposed any and all government intervention in markets. Although the Liberals had supported the repeal of the Corn Laws, they opposed any other measures that might have alleviated the crisis. Writing of Peel’s decision to import grain, Russell wrote: “It must be thoroughly understood that we cannot feed the people. It was a cruel delusion to pretend to do so.”

Contemporaries and historians have judged Russell’s blind adherence to economic orthodoxy harshly. One of the many coroner’s inquests that followed a famine death recommended that a charge of willful murder be brought against Russell for his refusal to intervene in the famine.

The euro was similarly the result of an ideologically based policy that was not supported by economic analysis.

In the aftermath of two world wars, many statesmen called for closer political and economic ties within Europe, including Winston Churchill, French premiers Edouard Herriot and Aristide Briand, and German statesmen Gustav Stresemann and Konrad Adenauer.

The post-World War II response to this desire for greater European unity was the European Coal and Steel Community, the European Economic Community, and eventually, the European Union each of which brought increasingly closer economic ties between member countries.

By the 1990s, European leaders had decided that the time was right for a monetary union and, with the Treaty of Maastricht (1993), committed themselves to the establishment of the euro by the end of the decade.

The leap from greater trade and commercial integration to a monetary union was based on ideological, rather than economic reasoning. Economists warned that Europe did not constitute an “optimal currency area,” suggesting that such a currency union would not be successful. The late German-American economist Rüdiger Dornbusch classified American economists as falling into one of three camps when it came to the euro: “It can’t happen. It’s a bad idea. It won’t last.”

The historical experience also suggested that monetary unions that precede political unions, such as the Latin Monetary Union (1865-1927) and the Scandinavian Monetary Union (1873-1914), were bound to fail, while those that came after political union, such as those in the United States in 18th century, Germany and Italy in the 19th century, and Germany in the 20th century were more likely to succeed. The various European Monetary System arrangements in the 1970s, none of which lasted very long, also provided evidence that European monetary unification was not likely to be smooth.

Concluding that it was a mistake to adopt the euro in the 1990s is, of course, not the same thing as recommending that the euro should be abandoned in 2014. German taxpayers have every reason to resent the cost of supporting their economically weaker—and frequently financially irresponsible—neighbors. However, Germany’s prosperity rests in large measure on its position as Europe’s most prolific exporter. Should Germany find itself outside the euro-zone, using a new, more expensive German mark, German prosperity would be endangered.

What we can say about the response to the Irish Famine and the decision to adopt the euro is that they were made for ideological, rather than economic reasons. These—and other episodes during the last 200 years—show that economic policy should never be made on the basis of economic ideology, but only on the basis of cold, hard economic analysis.

Subscribe to the OUPblog via email or RSS.

Subscribe to only business and economics articles on the OUPblog via email or RSS.

Image credits: (1) Irish potato famine, Bridget O’Donnel. Public domain via Wikimedia Commons. (2) Sir Robert Peel, portrait. Public domain via Wikimedia Commons.

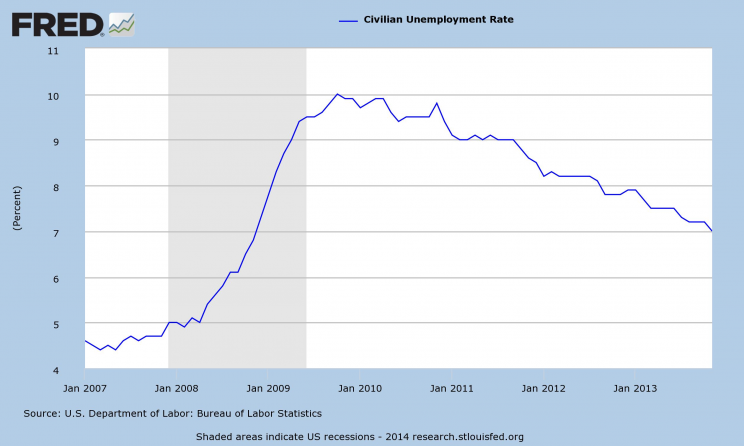

For the past half dozen years or so, the first Friday of the month has brought fear and dread to large portions of the United States. This heightened anxiety has nothing to do with the phases of the moon, the expiration of multiple financial derivatives, or concerns about not having a date for the weekend. No, at 8:30 am (Eastern Time) on the first Friday of each month, the US Bureau of Labor Statistics releases the unemployment data for the previous month.

The release of the unemployment data sets off a media frenzy, as pundits speculate on the winners and losers. What do the numbers foreshadow for the economy? Have we put the Great Recession behind us? How will Wall Street receive the news? And, perhaps most importantly, how does it affect the Administration’s popularity?

There are plenty of reasons why unemployment should be the “marquee” economic statistic. Unlike other important economic indicators, such as GDP, exports, and new housing starts, the human cost of unemployment is inescapable. On an aggregate level, every tenth of a percent increase in the unemployment rate represents about an additional 200,000 people out of work. It is a lot tougher to conjure up a picture of a 1.2 percent decline in GDP.

On the personal level, when unemployment touches our family, friends, and neighbors, it is hard to ignore.

The unemployment rate has been at the center of a monthly drama since the beginning of the Great Recession. As the economy worsened, the unemployment rate surged upward until it hit 10% of the workforce in October 2009, its highest rate in more than 25 years.

Data Source: FRED, Federal Reserve Economic Data, Federal Reserve Bank of St. Louis: Civilian Unemployment Rate (UNRATE); US Department of Labor: Bureau of Labor Statistics; accessed 19 May 2014.

With each uptick in unemployment, political analysts wondered out loud if the bad news spelled the failure of the Obama presidency…or the lengthening of the odds against his chances at a second term. For the Administration’s part, the chair of the President’s Council of Economic Advisors typically puts out a statement by 9:30 am on the day of the release, putting the best spin possible on the unemployment data.

Although the unemployment numbers have been and will remain an important economic indicator, in recent months their importance is being overshadowed by another statistic: inflation. There are a couple of reasons for this.

First, even though the unemployment rate has fallen consistently since November 2010, when it was 9.8%, until April 2014, when it was 6.3%, it is clear that the economy has not fully recovered from the Great Recession. Wage growth is anemic; there are still an alarming number of discouraged workers (who are no longer counted as unemployed because they have given up looking for work); and GDP growth is sluggish.

Second, despite the continuing weakness in the economy, lower unemployment has raised concerns that that the economy is overheating. Declining unemployment combined with several years of monetary stimulus via quantitative easing and other unconventional methods has led to concerns that inflation may emerge at any moment.

So far, there is little evidence that we are experiencing a sharp upturn in inflation. Nonetheless, concern that emerging inflation will force the Fed to undertake contractionary monetary policy which, in turn, may have adverse effects for both the high flying stock market and the still low flying economy, are now gaining ground.

Don’t expect the unemployment rate to sink into obscurity anytime soon. It has always been an important indicator of the health of the economy and will remain so. Just be prepared for a second media frenzy around the middle of each month—when the inflation indices are released.

Because Europe accounts for nearly a quarter of the world’s economic output, this question is important not only to Europeans, but to Africans, Asians, Americans (both North and South), and Australians as well. Those who forecast that the United States’s relatively anemic five-year-old recovery is poised to become stronger almost always include the caveat “unless, of course, Europe implodes.”

So, can we stop worrying about Europe?

Recent signs have been encouraging.

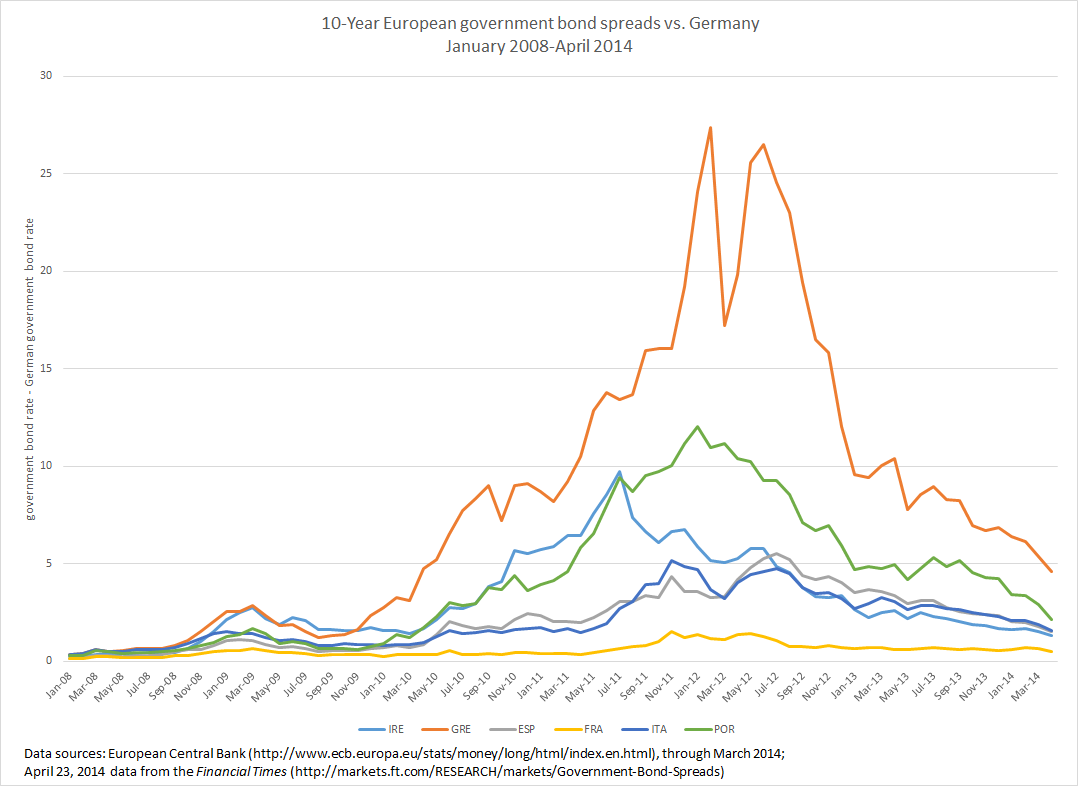

Consider the following graph, which shows the spread between the yields on the 10-year bonds of several European countries and those of the German government. Because the German government’s finances are relatively healthy—and Germany is thus viewed as being quite likely to pay back what it owes—it is able to borrow money more cheaply than most of its neighbors. For 10 years loans, the German government pays interest of about 1.5%, which is among the lowest rates in Europe.

Before the European sovereign debt crisis erupted 2009, spreads were not especially wide. In 2008, the Greek government paid between 0.25-0.75% more to borrow money for 10 years than the German government. When the sorry state of the Greek government’s finances became public, however, the spread between Greek and German yields soared to more than 20% and the European Union (EU) and the International Monetary Fund (IMF) were called in to bail out the Greek government. Ireland, Portugal, and Spain also received rescue packages (as did Cyprus), while Italy appeared to be headed down the same road. Note the wide spreads between these governments’ borrowing costs and those of the fiscally virtuous Germans.

During the last year or so, Greek, Irish, Portuguese, and Spanish spreads have shrunk considerably — not to their pre-crisis levels, but far below their sky-high levels of 2010-2012 — suggesting that doubts about the sustainability of European governments’ debts is receding. The decline in spreads is due in part to the austerity measures adopted as a condition of the EU/IMF bailouts, which have improved the budget outlook among the fiscally weaker countries. German Chancellor Angela Merkel’s April visit to Greece was widely seen as an effort to show support for fiscal austerity and economic restructuring adopted by the Greek Prime Minister Antonis Samaras.

Angela Merkel – Αντώνης Σαμαράς, 2012. Photo by Αντώνης Σαμαράς Πρωθυπουργός της Ελλάδας. CC BY-SA 2.0 via Wikimedia Commons.

In other positive news, Markit’s European purchasing manager’s composite index for March (released on 23 April 2014), which is considered a proxy for economic output, rose to a nearly three-year high. The index shows a continuous expansion of business activity since last July and forecasts that a backlog of work will lead to further growth in May.

Despite these positive signs, Europe is not out of the woods.

Unemployment remains stubbornly high, due, in part, to austerity: over 25% in Greece and Spain; over 15% in Portugal and Cyprus; and over 10% in France, Ireland, Italy, and a number of other countries.

Although prices are rising slightly in the European Union on average, Greece, Spain, Portugal and a few other European countries are experiencing deflation. Moreover, overall inflation in the EU is below that in the United States, leading the euro to appreciate by between 2-3% against the dollar since the beginning of 2014 and putting a crimp in European exports. Further, Europe’s flirtation with deflation increases the real burden on debtors. During inflationary times, debtors are able to repay their debts in money that is losing its value; deflation forces debtors to repay in money that is gaining in value.

The European economy is improving. But several indicators show that plenty can still go wrong. So let’s not stop worrying yet.

Subscribe to the OUPblog via email or RSS.

Subscribe to only business and economics articles on the OUPblog via email or RSS.

Image credit: Graph courtesy of Richard Grossman. Used with permission.

Russia’s seizure of Crimea from Ukraine has left its neighbors—particularly those with sizable Russian-speaking populations such as Kazakhstan, Latvia, Estonia, and what is left of Ukraine—looking over their shoulder wondering if they are next on Vladimir Putin’s list of territorial acquisitions. The seizure has also left Europe and United States looking for a coherent response.

Neither the Americans nor the Europeans will go to war over Crimea. Military intervention would be costly, unpopular at home, and not necessarily successful. Unless a fellow member of the North Atlantic Treaty Organization (which includes Latvia and Estonia) were attacked by Russia, thereby requiring a military response under the terms of the NATO treaty, the West will not go to war to check Putin’s land grabs.

So far, the West’s response—aside from harsh rhetoric—has been economic, not military. Both the United States and Europe have imposed travel and financial sanctions on a handful of close associates of Putin (which have had limited effect), with promises of escalation should Russia continue on its expansionist path.

What is the historical record on sanctions? And what are the chances for success if the West does escalate?

The earliest known use of economic sanctions was Pericles’s Megarian decree, enacted in 432 BCE, in which the Athenian leader “…banished [the Megarians] both from our land and from our markets and from the sea and from the continent” (Aristophanes, The Acharnians). The results of these sanctions, according to Aristophanes, was starvation among the Megarians.

Hufbauer, Schott, Elliot, and Oegg (2008) catalogue more than 170 instances of economic sanctions between 1910 and 2000. They find that only about one third of all sanctions efforts were even partially successful, although the success depends critically on the sanction’s goal. Limited goals (e.g. the release of a political prisoner) have been successful about half of the time; more ambitious goals (e.g. disruption of a military adventure, military impairment, regime change, or democratization) are successful between a fifth and a third of the time. Of course, these figures depend crucially on a whole host of additional factors, including the cost borne by the country imposing sanctions, the resilience of the country being sanctioned, and the necessity of international cooperation for the sanctions to be fully implemented.

Despite these cautionary statistics, sanctions can sometimes be effective. According to the US Congressional Research Service, recent US sanctions reduced Iranian oil exports by 60% and led to a decline in the value of the Iranian currency by 50%, forcing Iranian leaders to accept an interim agreement with the United States and its allies in November 2013. On the other hand, US sanctions against Cuba have been in place for more than 50 years and, although having helped to impoverish the island, they have not brought about the hoped for regime change.

Current thinking on sanctions favors what are known as “targeted” or “smart” sanctions. That is, rather than embargoing an entire economy (e.g. the US embargo of Cuba), targeted sanctions aim to hit particular individuals or sectors of the economy via travel bans, asset freezes, arms embargo, etc. Russian human rights campaigner and former World Chess Champion Gary Kasparov suggested in a Wall Street Journal opinion piece that the way to get to Putin through such smart sanctions, writing:

“If the West punishes Russia with sanctions and a trade war, that might be effective eventually, but it would also be cruel to the 140 million Russians who live under Mr. Putin’s rule. And it would be unnecessary. Instead, sanction the 140 oligarchs who would dump Mr. Putin in the trash tomorrow if he cannot protect their assets abroad. Target their visas, their mansions and IPOs in London, their yachts and Swiss bank accounts. Use banks, not tanks.”

If such sanctions were technically and legally possible—and that the expansionist urge comes from Putin himself and would not be echoed by his successor—this could be the quickest and most effective way to solve the problem.

A slower, but nonetheless sensible course is to squeeze Russia’s most important economic sector—energy. Russian energy exports in 2012 accounted for half of all government revenues. Sanctions that restrict Russia’s ability to export oil and gas would deal a devastating blow to the economy, which has already suffered from the uncertainty surrounding Russian intervention in Ukraine. By mid-March the Russian stock market was down over 10% for the year; the ruble was close to its record low against the dollar; and 10-year Russian borrowing costs were nearly 10%–more than 3% higher than those of the still crippled Greek economy—indicating that international lenders are already wary of the Russian economy.

A difficulty in targeting the Russian energy sector—aside from the widespread pain imposed on ordinary Russians–is that the Europeans are heavily dependent on it, importing nearly one third of their energy from Russia. Given the precarious position of its economy at the moment, an energy crisis is the last thing Europe needs. Although alternative energy sources not will appear overnight, old and new sources could eventually fill the gap, including greater domestic production and rethinking Germany’s plans to close its nuclear plants. Loosening export restrictions on the now-booming US natural gas industry would provide yet another alternative energy source to Europe and increase the effectiveness of sanctions. Freeing the industrialized world from dependence on dictators to fulfill their energy needs can only help the West’s long-term growth prospects and make it less susceptible to threats from rogue states.

If we are patient, squeezing Russia’s energy sector might work. In the short run, however, sanctioning the oligarchs may be the West’s best shot.

Subscribe to the OUPblog via email or RSS.

Subscribe to only business and economics articles on the OUPblog via email or RSS.

Image credits: (1) Vladimir Putin. Russian Presidential Press and Information Office. CC BY 3.0 by kremlin.ru. (2) Abrakupchinskaya oil exploration drilling rig in Evenkiysky District. Photo by ShavPS. CC-BY-SA-3.0 via Wikimedia.

Neither the Americans nor the Europeans will go to war over Crimea. Military intervention would be costly, unpopular at home, and not necessarily successful. Unless a fellow member of the North Atlantic Treaty Organization (which includes Latvia and Estonia) were attacked by Russia, thereby requiring a military response under the terms of the NATO treaty, the West will not go to war to check Putin’s land grabs.

Neither the Americans nor the Europeans will go to war over Crimea. Military intervention would be costly, unpopular at home, and not necessarily successful. Unless a fellow member of the North Atlantic Treaty Organization (which includes Latvia and Estonia) were attacked by Russia, thereby requiring a military response under the terms of the NATO treaty, the West will not go to war to check Putin’s land grabs. A slower, but nonetheless sensible course is to squeeze Russia’s most important economic sector—energy.

A slower, but nonetheless sensible course is to squeeze Russia’s most important economic sector—energy.