new posts in all blogs

Viewing: Blog Posts Tagged with: banking, Most Recent at Top [Help]

Results 1 - 13 of 13

How to use this Page

You are viewing the most recent posts tagged with the words: banking in the JacketFlap blog reader. What is a tag? Think of a tag as a keyword or category label. Tags can both help you find posts on JacketFlap.com as well as provide an easy way for you to "remember" and classify posts for later recall. Try adding a tag yourself by clicking "Add a tag" below a post's header. Scroll down through the list of Recent Posts in the left column and click on a post title that sounds interesting. You can view all posts from a specific blog by clicking the Blog name in the right column, or you can click a 'More Posts from this Blog' link in any individual post.

By: Fiona Parker,

on 12/22/2015

Blog:

OUPblog

(

Login to Add to MyJacketFlap)

JacketFlap tags:

Oxford Law Vox,

bank resolution,

Deposit Protection and Bank Resolution,

financial crisis 2008,

regulatory regimes,

Nikoletta Kleftouri,

bank failure,

deposit protection,

Northern Rock,

Vickers' Report,

podcast,

Books,

Law,

Finance,

*Featured,

Audio & Podcasts,

Business & Economics,

banking,

policy,

financial crisis,

financial regulation,

commercial law,

Add a tag

In this episode of the Oxford Law Vox podcast, banking law expert Nikoletta Kleftouri talks to George Miller about banking law issues today. Together they discuss some of the major legal and policy issues that arose from the financial crisis in 2008, including assessing systemic risk and whether the notion of “too big to fail” is on the road to extinction.

The post Oxford Law Vox: deposit protection and bank resolution appeared first on OUPblog.

By: DanP,

on 8/5/2015

Blog:

OUPblog

(

Login to Add to MyJacketFlap)

JacketFlap tags:

dollar bills,

dollar coins,

Books,

Economics,

money,

dollars,

Finance,

banking,

economy,

*Featured,

Business & Economics,

US economy,

Richard S. Grossman,

Economic Policy with Richard S. Grossman,

Wrong nine economic policy disasters,

Add a tag

The next time you are slipping the valet a couple of folded dollar bills, take a good look at those George Washingtons. You might never see them again. Every few years, there is a renewed push for the United States to replace the dollar bill with its shiny cousin, the one dollar coin.

The post A fist-full of dollar bills appeared first on OUPblog.

By: DanP,

on 7/1/2015

Blog:

OUPblog

(

Login to Add to MyJacketFlap)

JacketFlap tags:

Books,

Economics,

business,

Finance,

banking,

economy,

economists,

Social Sciences,

*Featured,

Business & Economics,

Richard S. Grossman,

Economic Policy with Richard S. Grossman,

economic policy,

Wrong nine economic policy disasters,

uk economics,

economic policy with richard grossman,

us economics,

european economics,

regulatory cooperation,

Add a tag

One of the most striking structural weaknesses uncovered by the euro crisis is the lack of consistent banking regulation and supervision in Europe. Although the European Banking Authority has existed since 2011, its influence is often trumped by national authorities. And many national governments within the European Union do not seem anxious to submit their financial institutions to European-wide regulation and supervision.

The post The limits of regulatory cooperation appeared first on OUPblog.

By:

keilinh,

on 10/21/2014

Blog:

The Open Book

(

Login to Add to MyJacketFlap)

JacketFlap tags:

Economics,

money,

Paula Yoo,

banking,

banks,

loans,

Musings & Ponderings,

nobel peace prize,

Muhammad Yunus,

bangladesh,

Lee & Low Likes,

Guest Blogger Post,

grameen bank,

loan shark,

microcredit,

poverty,

Add a tag

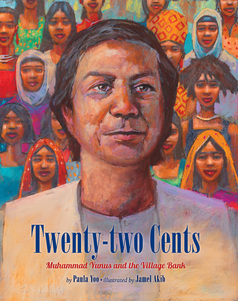

Paula Yoo is a children’s book writer, television writer, and freelance violinist living in

Paula Yoo is a children’s book writer, television writer, and freelance violinist living in Los Angeles. Her latest book, Twenty-two Cents: Muhammad Yunus and the Village Bank, was released last month. Twenty-two Cents is about Muhammad Yunus, Nobel Peace Prize winner and founder of Grameen Bank. He founded Grameen Bank so people could borrow small amounts of money to start a job, and then pay back the bank without exorbitant interest charges. Over the next few years, Muhammad’s compassion and determination changed the lives of millions of people by loaning the equivalent of more than ten billion US dollars in micro-credit. This has also served to advocate and empower the poor, especially women, who often have limited options. In this post, we asked her to share advice on what’s she’s learned about banking, loans, and managing finances while writing Twenty-two Cents.

Los Angeles. Her latest book, Twenty-two Cents: Muhammad Yunus and the Village Bank, was released last month. Twenty-two Cents is about Muhammad Yunus, Nobel Peace Prize winner and founder of Grameen Bank. He founded Grameen Bank so people could borrow small amounts of money to start a job, and then pay back the bank without exorbitant interest charges. Over the next few years, Muhammad’s compassion and determination changed the lives of millions of people by loaning the equivalent of more than ten billion US dollars in micro-credit. This has also served to advocate and empower the poor, especially women, who often have limited options. In this post, we asked her to share advice on what’s she’s learned about banking, loans, and managing finances while writing Twenty-two Cents.

What are some reasons why someone might want to take out a loan? Why wouldn’t banks loan money to poor people in Bangladesh?

PAULA: People will take out a loan when they do not have enough money in their bank account to pay for a major purchase, like a car or a house. Sometimes, they will take out a loan because they need the money to help set up a business they are starting. Other times, loans are also used to help pay for major expenses, like unexpected hospital bills for a family member who is sick or big repairs on a house or car. But asking for a loan is a very complicated process because a person has to prove they can pay the loan back in a reasonable amount of time. A person’s financial history can affect whether or not they are approved for a loan. For many people who live below the poverty line, they are at a disadvantage because their financial history is very spotty. Banks may not trust them to pay the loan back on time.

In addition, most loans are given to people who are requesting a lot of money for a very expensive purchase like a house or a car. But sometimes a person only needs a small amount of money – for example, a few hundred dollars. This type of loan does not really exist because most people can afford to pay a few hundred dollars. But if you live below the poverty line, a hundred dollars can seem like a million dollars. Professor Yunus realized this when he met Sufiya Begum, a poor woman who only needed 22 cents to keep her business of making stools and mats profitable in her rural village. No bank would loan a few hundred dollars, or even 22 cents, to a woman living in a mud hut. This is what inspired Professor Yunus to come up with the concept of “microcredit” (also known as microfinancing and micro banking).

In TWENTY-TWO CENTS, microcredit is described as a loan with a low interest rate. What is a low interest rate compared to a high interest rate?

PAULA: When you borrow money from a bank, you have to pay the loan back with an interest rate. The interest rate is an additional amount of money that you now owe the bank on top of the original amount of money you borrowed. There are many complex math formulas involved with calculating what a fair and appropriate interest rate could be for a loan. The interest rate is also affected by outside factors such as inflation and unemployment. Although it would seem that a lower interest rate would be preferable to the borrower, it can be risky to the general economy. A low interest rate can create a potential “economic bubble” which could burst in the future and cause an economic “depression.” Interest rates are adjusted to make sure these problems do not happen. Which means that sometimes there are times when the interest rates are higher for borrowers than other times.

What is a loan shark?

PAULA: A loan shark is someone who offers loans to poor people at extremely high interest rates. This is also known as “predatory lending.” It can be illegal in several cases, especially when the loan shark uses blackmail or threats of violence to make sure a person pays back the loan by a certain deadline. Often people in desperate financial situations will go to a loan shark to help them out of a financial problem, only to realize later that the loan shark has made the problem worse, not better.

Did your parents explain how a bank works to you when you were a child? Or did you learn about it in school?

PAULA: I remember learning about how a bank works from elementary school and through those “Schoolhouse Rocks!” educational cartoons they would show on Saturday mornings. But overall, I would say I learned about banking as a high school student when I got my first minimum wage job at age 16 as a cashier at the Marshall’s department store. I learned how banking worked through a job and real life experience.

TWENTY-TWO CENTS is a story about economic innovation. Could you explain why Muhammad Yunus’s Grameen Bank was so innovative or revolutionary?

PAULA ANSWER: Muhammad Yunus’ theories on microcredit and microfinancing are revolutionary and innovative because they provided a practical solution on how banks can offer loans to poor people who do not have any financial security. By having women work together as a group to understand how the math behind the loan would work (along with other important concepts) and borrowing the loan as a group, Yunus’ unique idea gave banks the confidence to put their trust into these groups of women. The banks were able to loan the money with the full confidence in knowing that these women would be able to pay them back in a timely manner. The humanitarian aspect of Yunus’ economic theories were also quite revolutionary because it gave these poverty-stricken women a newfound sense of self-confidence. His theories worked to help break the cycle of poverty for these women as they were able to save money and finally become self-sufficient. The Nobel Committee praised Yunus’ microcredit theories for being one of the first steps towards eradicating poverty, stating, “Lasting peace cannot be achieved unless large population groups find ways in which to break out of poverty.”

Twenty-two Cents: Muhammad Yunus and the Village Bank is a biography of 2006 Nobel Peace Prize winner Muhammad Yunus, who founded Grameen Bank and revolutionized global antipoverty efforts by developing the innovative economic concept of micro-lending.

Twenty-two Cents: Muhammad Yunus and the Village Bank is a biography of 2006 Nobel Peace Prize winner Muhammad Yunus, who founded Grameen Bank and revolutionized global antipoverty efforts by developing the innovative economic concept of micro-lending.

Filed under: Guest Blogger Post, Lee & Low Likes, Musings & Ponderings Tagged: bangladesh, banking, banks, Economics, grameen bank, loan shark, loans, microcredit, money, Muhammad Yunus, nobel peace prize, Paula Yoo, poverty

By: Kirsty,

on 4/16/2014

Blog:

OUPblog

(

Login to Add to MyJacketFlap)

JacketFlap tags:

Humanities,

french literature,

Emile Zola,

*Featured,

zola,

rougon-macquart,

saccard,

bourse,

sigismond,

Literature,

money,

paris,

translation,

Finance,

OWC,

banking,

Oxford World's Classics,

Add a tag

By Valerie Minogue

Money is a tricky subject for a novel, as Zola in 1890 acknowledged: “It’s difficult to write a novel about money. It’s cold, icy, lacking in interest…” But his Rougon-Macquart novels, the “natural and social history” of a family in the Second Empire, were meant to cover every significant aspect of the age, from railways and coal-mines to the first department stores. Money and the Stock Exchange (the Paris Bourse) had to have a place in that picture, hence Money, the eighteenth of Zola’s twenty-novel cycle.

The subject is indeed challenging, but it makes an action-packed novel, with a huge cast, led by a smaller group of well-defined and contrasting characters, who inhabit a great variety of settings, from the busy, crowded streets of Paris to the inside of the Bourse, to a palatial bank, modest domestic interiors, houses of opulent splendour — and a horrific slum of filthy hovels that makes a telling comment on the social inequalities of the day.

Dominating the scene from the beginning is the central, brooding figure of Saccard. Born Aristide Rougon, Saccard already appears in earlier novels of the Rougon-Macquart, notably in The Kill, which relates how Saccard, profiting from the opportunities provided by Haussman’s reconstruction of Paris, made – and lost – a huge fortune in property deals. Money relates Saccard’s second rise and fall, but Saccard here is a more complex and riveting figure than in The Kill.

Émile Zola painted by Edouard Manet

It is Saccard who drives all the action, carrying us through the widely divergent social strata of a time that Zola termed “an era of folly and shame”, and into all levels of the financial world. We meet gamblers and jobbers, bankers, stockbrokers and their clerks; we get into the floor of the Bourse, where prices are shouted and exchanged at break-neck speed, deals are made and unmade, and investors suddenly enriched or impoverished. This is a world of insider-trading, of manipulation of share-prices and political chicanery, with directors lining their pockets with fat bonuses and walking off wealthy when the bank goes to the wall — scandals, alas, so familiar that it is hard to believe this book was written back in 1890! Saccard, with his enormous talent for inspiring confidence and manipulating people, would feel quite at home among the financial operators of today.

Saccard is surrounded by other vivid characters – the rapacious Busch, the sinister La Méchain, waiting vulture-like for disaster and profit, in what is, for the most part, a morally ugly world. Apart from the Jordan couple, and Hamelin and his sister Madame Caroline, precious few are on the side of the angels. But there are contrasts not only between, but also within, the characters. Nothing and no-one here is purely wicked, nor purely good. The terrible Busch is a devoted and loving carer of his brother Sigismond. Hamelin, whose wide-ranging schemes Saccard embraces and finances, combines brilliance as an engineer with a childlike piety. Madame Caroline, for all her robust good sense, falls in love with Saccard, seduced by his dynamic vitality and energy, and goes on loving him even when in his recklessness he has lost her esteem. Saccard himself, with all his lusts and vanity and greed, works devotedly for a charitable Foundation, delighting in the power to do good.

Money itself has many faces: it’s a living thing, glittering and tinkling with “the music of gold”, it’s a pernicious germ that ruins everything it touches, and it’s a magic wand, an instrument of progress, which, combined with science, will transform the world, opening new highways by rail and sea, and making deserts bloom. Money may be corrupting but is also productive, and Saccard, similarly – “is he a hero? is he a villain?” asks Madame Caroline; he does enormous damage, but also achieves much of real value.

Fundamental questions about money are posed in the encounter between Saccard and the philosopher Sigismond, a disciple of Karl Marx, whose Das Kapital had recently appeared — an encounter in which individualistic capitalism meets Marxist collectivism head to head. Both men are idealists in very different ways, Sigismond wanting to ban money altogether to reach a new world of equality and happiness for all, a world in which all will engage in manual labour (shades of the Cultural Revolution!), and be rewarded not with evil money but work-vouchers. Saccard, seeing money as the instrument of progress, recoils in horror. For him, without money, there is nothing.

If Zola vividly presents the corrupting power of money, he also shows its expansive force as an active agent of both creation and destruction, like an organic part of the stuff of life. And it is “life, just as it is” with so much bad and so much good in it, that the whole novel finally reaffirms.

Valerie Minogue has taught at the universities of Cardiff, Queen Mary University of London, and Swansea. She is co-founder of the journal Romance Studies and has been President of the Émile Zola Society, London, since 2005. She is the translator of the new Oxford World’s Classics edition of Money by Émile Zola.

For over 100 years Oxford World’s Classics has made available the broadest spectrum of literature from around the globe. Each affordable volume reflects Oxford’s commitment to scholarship, providing the most accurate text plus a wealth of other valuable features, including expert introductions by leading authorities, voluminous notes to clarify the text, up-to-date bibliographies for further study, and much more. You can follow Oxford World’s Classics on Twitter, Facebook, or here on the OUPblog.

Subscribe to the OUPblog via email or RSS.

Subscribe to only Oxford World’s Classics articles on the OUPblog via email or RSS.

Subscribe to only literature articles on the OUPblog via email or RSS.

Image credit: Émile Zola by Edouard Manet [public domain] via Wikimedia Commons.

The post Money matters appeared first on OUPblog.

By: Alice,

on 1/31/2013

Blog:

OUPblog

(

Login to Add to MyJacketFlap)

JacketFlap tags:

Current Affairs,

markets,

banking,

taxpayers,

credit crunch,

banks,

shareholders,

*Featured,

Law & Politics,

Business & Economics,

LIBOR,

European Monetary mechanism,

Financial Markets and Exchanges Law,

George Walker,

investment markets,

Michael Blair QC,

public backlash,

Stuart Willey,

Vickers reforms,

willey,

Add a tag

By Michael Blair QC, George Walker, and Stuart Willey

Almost every day has brought a fresh story about investment markets, their strengths and weaknesses. Misreporting of data for calculation of LIBOR, money laundering with a whiff of Central American drugs trading, costly malfunctioning of programme trading mechanisms which brought the trading company to its knees, reputational damage inflicted by as yet unsubstantiated accusations of illicit financing in breach of international sanctions… the list goes on and on.

Toronto Financial District. Photo by Alessio Bragadini, 23 June 2009. Creative Commons License.

And this has all been on top of the recent history of the so-called

credit crunch and the self-inflicted wounds that have beset the banking industry over the last five years, with consequentially a savage public backlash of distrust and dislike of bankers and banks. This has affected the banking fraternity as a whole, even though those that caused the damage to their banks, to the shareholders and in the end to the taxpayers, were a small sub-set only of the banking workforce.

The list of problems, for firms, and in some cases for their customers as well, prompts some reflections about the role of investment markets in our society and about the relationship between markets and their regulation. Some years ago, in the latter part of the last century, it was fashionable for academics and practitioners alike to put their trust in the strength and reliability of market mechanisms. The experience in earlier decades of the hard discipline of the money markets no doubt added to this. For example the humiliation of the forced departure of the United Kingdom from the former European Monetary mechanism (EMU) in the 1980s reinforced the beliefs of many in the power of the markets as a way of finding and pricing out inefficiency and restoring a new equilibrium at a different point on the scale.

To the majority, therefore, the proper role of regulation at that time was essentially limited to cases of market failure. Most of the work in the public interest could be done by the markets themselves. They might, of course, need some help from the regulators to ensure proper disclosure, with a view to sufficient, and non-discriminatory, access by market users and commentators to market information. But if there was “sunlight” in the market, then that more or less guaranteed the “hygiene” of its mechanisms. From that concept came “light touch” as a means of describing a system of financial regulation that basically left it to well informed markets to function for themselves.

Not all agreed at the time with this general approach. There were honourable exceptions, whose only consolation since has been the (frequently best left unsaid) phrase “I told you so at the time”.

How things have changed since then! A rapid U-turn in public and political thinking has brought demands for sterner and more intrusive regulation. The insidiousness of human greed and of lack of foresight is now widely recognised and needs to be restrained. The market economists now accept that there is a real, and central, role for discipline, including both its punitive and its deterrent aspects as well as the benefits it brings in excluding the dangerous from the playing field altogether. The change has even led our politicians to embark on structural change to restore a previous splitting of retail regulation from the upper reaches of financial services. The case for this change has been based on a hope of better focus of the two new bodies on the two sectors, though the underlying motive appears more to be a desire to change something simply because it is thought to have failed.

Splitting in the public interest also seems likely to be required in the major banks as well. The “Vickers” reforms look set to require the banking industry to function in two separate ways, with required distance between the investment banking arms and the general consumer-based borrowing and lending functions.

Another consequence is that “enforcement” is once more central to the world of regulation, rather than seen as a stick kept, as far as was possible, in the cupboard for occasional use only in the most serious circumstances.

We have now arrived at a new post-crisis period of great challenge but also of potential opportunity. We seem to be set for a number of difficult coming years, during which the markets will be dominated and constrained by austerity, continuing uncertainty and risks of instability. But markets and economies tend to recover over time. We must hope that the politicians, central banks and regulatory authorities have learned all of the necessary lessons from the recent crises to prevent instability or, at least, better to manage and contain the risks of it.

Michael Blair QC, Professor George Walker, and Stuart Willey are the editors of the new edition of Financial Markets and Exchanges Law. Michael Blair QC is in independent practice at the Bar of England and Wales specialising in financial services. Previously General Counsel to the Board of the Financial Services Authority. Queen’s Counsel honoris causa 1996. George Walker is Professor in International Financial Law at School of Law, Queen Mary University of London and is a member of the Centre for Commercial Law Studies (CCLS). He is also a Barrister and Member of the Honourable Society of Inner Temple in London. Stuart Willey is Counsel and Head of the Regulatory Practice in the Banking & Capital Markets group of White & Case in London. Stuart specializes in financial regulation focusing on the securities markets, banking and insurance.

Subscribe to the OUPblog via email or RSS.

Subscribe to only law and politics articles on the OUPblog via email or RSS.

The post Understanding and respecting markets appeared first on OUPblog.

By: Anastasia Goodstein,

on 12/1/2011

Blog:

Ypulse

(

Login to Add to MyJacketFlap)

JacketFlap tags:

banking,

Mariah Carey,

Stan Lee,

macy's,

dosomething.org,

big mac,

folk music,

qr codes,

justin bieber,

willow smith,

living social,

all i want for christmas,

disney reads,

grammy nominations,

ocbc bank,

snap codes,

teens and texting,

the amazing spider-man: an origin story,

McDonald's,

Add a tag

Disney has debuted a new social media initiative called Disney Reads (spanning Facebook, Twitter, and YouTube. We love that they’re posting sweepstakes, contests, quizzes, and other exclusive content, but we’re a little perplexed at... Read the rest of this post

Disney has debuted a new social media initiative called Disney Reads (spanning Facebook, Twitter, and YouTube. We love that they’re posting sweepstakes, contests, quizzes, and other exclusive content, but we’re a little perplexed at... Read the rest of this post

It's

Nonfiction Monday and I'm back from my vacation to Boston, a wonderful city which lays claim to the title of Birthplace of America. The role of Boston in the American Revolution cannot be denied, nor can the contributions of Alexander Hamilton, scholar, soldier, politician and statesman.

Frtiz, Jean. 2011.

Alexander Hamilton: The Outsider. New York: Putnam.

In

Alexander Hamilton: The Outsider, Jean Fritz follows a theme that ran through all aspects of Hamilton's life - that of outsider. Born on the island of St. Kitts in the West Indies, Hamilton was often accused of being an interloper in Revolutionary American politics. Once committed to the ideal of a free and independent America, however, his "outsider" status never dampened his enthusiasm for his country. Fritz recounts his many contributions to the revolutionary cause and to these United States.

Besides serving in the Revolutionary War, he was also an aide-de-camp to then General George Washington. He served as a New York delegate to the Constitutional Convention. He was the architect of the Bank of the United States and the nation's first Secretary of the Treasury. As a New Jerseyan, I knew that his life ended in Weehawken in the famous duel with Aaron Burr, but I did not know that he founded the city of Paterson. He was convinced that American should and would be more than an agrarian society. He chose Paterson because its large waterfall could be used to generate electricity for business. (In 2009,

Paterson's Great Falls became a National Park Historic District)

In short, using her customary exactitude, Fritz tells a complete story of a complex man, using only facts and period quotations in this small, slim, 144-page volume. Archaic language ("poltroon") or long-abandoned customs (anonymous leaflet writing) are explained fully in the author's Notes. Historical reproductions (credited) are scattered throughout. A Bibliography and extensive Index complete the book.

This would make an excellent choice for a school biography report, much better than the formulaic series that students often choose.

The United States Treasury website features a page on Alexander Hamilton, the nation's first Secretary of the Treasury, and architect of the National Bank and the US Mint.Just an aside - Jean Fritz is 95 years old! How wonderful that she's still working and producing great children's books.

Today's Nonfiction Monday roundup is at

Telling the Kids the Truth: Writing Nonfiction for Children. Please

Scott Shane is an angel investor with the North Coast Angel Fund, and a professor of entrepreneurship at Case Western Reserve University. In his book Fool’s Gold: The Truth Behind Angel Investing in America he draws on hard data from the Federal Reserve and other sources to pain the first reliable group portrait of the lionized angel investors. Below is an excerpt from the beginning of the book which gives a simple explanation of what angel investors are.

…An angel investor is a person who provides capital, in the form of debt or equity, from his own funds to a private business owned and operated by someone else, who is neither a friend nor family member.

Business angels are far from the only source of external capital that entrepreneurs can tap. The entrepreneurs’ friends and family, venture capitalists, banks, trade creditors, credit card companies, and a host of other entities provide capital to private business.

To minimize the confusion about which capital sources are angel investors, I’m also going to defne some other sources of funds for private companies:

- Institutional investor: A corporation, financial institution, or other organization (e.g., venture capital firm) that uses money raised from another party to provide capital to a private business owned and operated by someone else.

- Friends and family investor: An individual who uses his own money to provide capital to a private business owned and operated by a family member, work colleague, friend or neighbor.

- Informal investor: An individual (not an institution) who uses his own money to provide capital to a private business owned and operated by someone else.

These definitions make it clear that the term “angel investor” is not synonymous with the term “informal investor”. Rather, angel investors are a subset of all informal investors, which include friends-and-family investors. That is, every angel is an informal investor, but not every informal investor is an angel; and individuals who make angel investments can, and do, make friends-and-family investments as well. Translated into more common parlance, informal investors encompass the three F’s-friends, family, and fools (angels).

I love that my bank is making it easier for me to do business with them by no longer requiring me to put deposits in envelopes. I can just imagine the committee meetings for this one:

- But we’ve never done that before.

- But it will mean more work for our staff.

- But we don’t know what crazy thing might happen.

- And on and on

This makes my user experience easier and more convenient, which I really appreciate. And of course, those who still want to use envelopes can do so.

What small things can your library do to make your services (both in your building and online) easier and more convenient for your users?

banking,

convenience,

library 2.0,

user centered

By: Rebecca,

on 4/2/2008

Blog:

OUPblog

(

Login to Add to MyJacketFlap)

JacketFlap tags:

shopping,

cards,

Media,

cash,

card,

swipe,

credit,

debt,

banking,

stuart,

vyse,

Add a tag

Stuart Vyse is Professor of Psychology at Connecticut College, in New London. In his new book, Going Broke: Why Americans Can’t Hold On To Their Money, he offers a unique psychological perspective on the financial behavior of the many Americans today who find they cannot make ends meet, illuminating the causes of our wildly self-destructive spending habits. In the article below he looks at how credit cards lead to debt problems. Read Vyse’s other posts here.

Suddenly cash isn’t quick enough for our fast-paced world. If you want to be happy and efficient and avoid the critical stares of cashiers and fellow customers, you need to swipe or tap a card and keep the line moving. According to the latest round of credit card commercials, checks and cash are just so 20th Century. (more…)

Share This

By: Rebecca,

on 9/11/2007

Blog:

OUPblog

(

Login to Add to MyJacketFlap)

JacketFlap tags:

sark,

channel,

feudalism,

carts,

locomotion,

microstates,

principalities,

blog,

oxford,

Geography,

maps,

A-Featured,

Ben's Place of the Week,

atlas,

ben,

bicycles,

keene,

Add a tag

Sark, United Kingdom

Coordinates: 49 25 N 2 22 W

Approximate area: 2 square miles (5 sq km)

Times change, and with them, people and places are carried along on the tide of modernization. But not always. On the tiny island of Sark in the English Channel, feudalism has clung, virtually unnoticed, to its rocky shores since the Middle Ages. In fact, this hereditary form of rule hung on long enough to make it the only feudal territory left on Europe, a continent known (among political geographers at least) for its microstates and puny principalities. (more…)

Share This

Wow! I learned some new things about him just from the posts. i think this would be an interesting biography to check out.

I've added it to my cart--I love these kinds of biographies. Plus it is long enough for all the teachers that want 100+ pages.